Overview:

Grantor Retained Annuity Trusts (“GRATs”) remain one of the most common estate planning strategies for transferring wealth while retaining cash flow and minimizing gift tax exposure. By design, GRATs allow investors to shift future appreciation – and importantly, excess yield – out of their taxable estate, making them particularly compelling in environments where assets generate strong or above-market returns.

For investors holding high-yielding or appreciating assets, GRATs offer a disciplined framework to convert return potential into generational wealth transfer.

How GRATs Work:

A GRAT is an irrevocable trust in which a grantor contributes assets while retaining a fixed annuity payment for a defined term. At the end of that term, any remaining value in the trust passes to beneficiaries, either outright or in further trust.

The strategy hinges on the IRS Section 7520 rate (the “hurdle rate”, currently 4.6%), which represents the IRS’s assumed yield on trust assets for gift tax purposes. If the assets in the GRAT outperform this rate, the excess value transfers to heirs—often with minimal or no gift tax.

This limited downside but potential meaningful upside transfer, drives the strategy’s appeal.

Why GRATs Are Attractive for High-Yielding Assets:

GRATs are most effective when funded with assets generating returns meaningfully above the IRS hurdle rate. This dynamic makes them particularly attractive for high-yielding investments, including private credit, structured income strategies, and other income-oriented assets.

Key advantages include:

❑ Consistent Outperformance Potential: Income-generating assets (e.g., private credit, structured investments) can more reliably exceed the Section 7520 rate,

❑ Cash Flow to Support Annuities: Yield helps fund required annuity payments without eroding principal,

❑ Accelerated Wealth Transfer: Excess income and reinvested returns compound within the trust, increasing the remainder to beneficiaries.

A GRATs success requires that the rate of return must exceed the IRS §7520 rate, reinforcing the importance of selecting assets with durable yield and return characteristics.

IN LOW-RATE ENVIRONMENTS – HISTORICALLY, A SWEET SPOT FOR GRATS – EVEN MODESTLY HIGH-YIELDING ASSETS CAN GENERATE SIGNIFICANT EXCESS TRANSFER VALUE.

Key Considerations and Risks:

While GRATs offer compelling benefits, their success depends on careful structuring and execution, and consideration of the following:

- Mortality Risk: If the grantor does not survive the GRAT term, assets will be included in the grantor’s estate for estate tax purposes,

- Performance Risk: If assets fail to outperform the hurdle rate, little or no wealth is transferred,

- Generation Skipping Transfer Tax Limitations: GRATs are not inherently efficient for generation-skipping transfer tax planning.

Structuring Alternatives:

Several structuring alternatives can enhance a GRAT’s effectiveness:

❑ Zeroed-Out GRATs: Designed so that the present value of annuity payments equals the contributed assets, minimizing the grantor’s taxable gift,

❑ Escalating Annuity GRATs: Annuity payments can be structured to increase 20% each year, resulting in lower annuity payments in early years and potentially leaving more appreciation within the GRAT, and remaining at the end of the GRAT term to pass to heirs gift tax free.

❑ Rolling GRATs: A series of short-term GRATs can reduce mortality risk and capture appreciation over time,

❑ Term: Shorter terms reduce estate inclusion risk, while longer terms may increase upside.

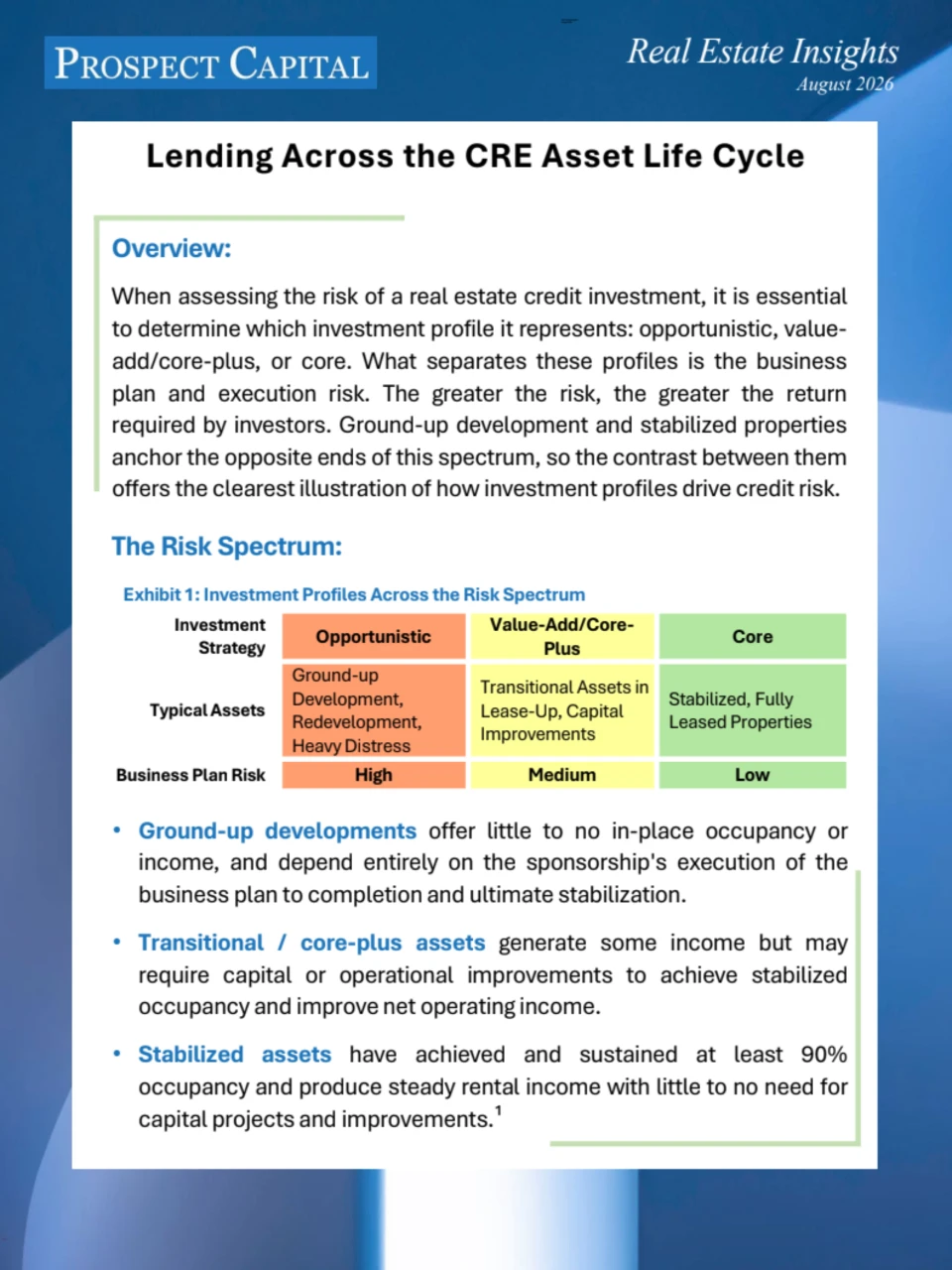

Asset Selection: The Primary Driver of Success

The choice of assets remains the most critical determinant of a GRAT’s outcome. As noted, assets with strong appreciation potential or consistent income generation are best suited for GRAT funding, while low-growth or depreciating assets are less effective.

Conclusion

GRATs remain a powerful estate planning tool, especially in environments where investors have access to high-yielding, income-generating assets capable of outperforming IRS benchmark rates.

Estate Planning Insights

BY COMBINING PREDICTABLE ANNUITY PAYMENTS WITH THE ABILITY TO TRANSFER EXCESS RETURNS TAX-EFFICIENTLY, GRATS OFFER A COMPELLING FRAMEWORK FOR LONG-TERM WEALTH TRANSFER.

Disclosures

Past Performance is not indicative of future results

Institutional Use Only

Prospect Capital Management L.P. (“Prospect”) is an SEC registered investment adviser that was founded in 1988 (along with its predecessors). Prospect invests across the United States in diversified portfolios by industry, company, and situation, and its proprietary underwriting process and metrics have been developed over more than 30 years and through multiple economic cycles. Prospect has over 150 employees and $9.6 billion** of assets under management as of December 31, 2025. With a buy-and-hold mentality, Prospect’s objectives are to preserve capital by making credit and equity-focused investments at reasonable multiples of recurring cash flow, earn attractive current cash yields and long-term capital appreciation while achieving consistent low-volatility returns. For more information, call 212.448.0702 or visit prospectcap.com

**The $9.6 billion of Assets Under Management (“AUM”) refers to the assets managed by Prospect and its affiliated registered investment advisors. AUM equals the sum of: (i) the gross assets of (a) Prospect Capital Corporation (“PSEC”), Priority Income Fund, Inc. (“PRIS”), Prospect Floating Rate and Alternative Income Fund, Inc. (“PFLOAT”), Prospect Credit REIT, LLC (“PCRED”), and Prospect Enhanced Yield Fund (“PENF”), and (b) pooled investment vehicles with respect to discrete assets for which Prospect has non-discretionary authority, (ii) any amounts available to be borrowed under certain credit facilities of the investment companies, (iii) total managed assets for real estate and structured credit investments, and (iv) uncalled capital commitments. Prospect’s AUM measure includes assets under management for which Prospect charges either nominal or zero fees. Prospect’s definition of AUM is not based on any definition of assets under management contained in any management agreements of the investment companies Prospect manages. Given the differences in the investment strategies and structures among other investment advisors, Prospect’s calculation of AUM may differ from the calculations employed by other investment managers and, as a result, this measure may not be directly comparable to similar measures presented by other investment managers. Prospect’s calculation also differs from the manner in which Prospect and its affiliates registered with the SEC report “Regulatory Assets Under Management” ($7.2 billion) on Form ADV.

This information is educational in nature and does not constitute an offer to sell or the solicitation of an offer to buy any securities. Prospect is not adopting, making a recommendation for or endorsing any investment strategy or particular security. All opinions are subject to change without notice, and you should always obtain current information and perform due diligence before participating in any investment. All investing is subject to risk, including the possible loss of principal. Prospect cannot guarantee that the information herein is accurate, complete or timely. We make no representation or warranty in respect of any information derived from the third-party sources which has not been independently verified. Prospect and its affiliates do not provide tax, legal or accounting advice. This material is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.