Collateralized Loan Obligations, or CLOs, have historically been the largest source of demand for leveraged loans in the U.S. market,¹ but they are largely ignored by mainstream financial news media and are still considered a niche product by many. We believe that the lack of attention to the asset class is not only a missed opportunity for businesses seeking new sources of funding, but also for investors seeking exposure to diversified corporate credit.

The Leveraged Loan Market & CLO Demand

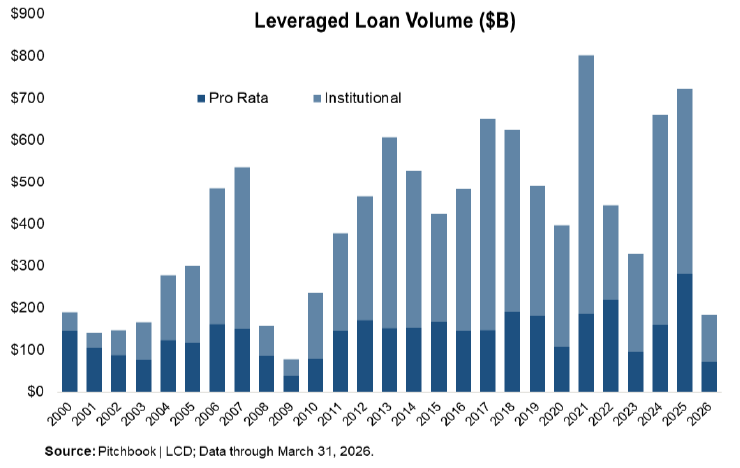

There are thousands of U.S. companies whose debt trades in the leveraged loan market, with total new issuance volume reaching $721 billion in 2025.²

Leveraged loan borrowers span healthcare, technology, industrials, consumer goods, and nearly every other sector, and range from established middle-market companies to large multinational corporations. These loans may offer an attractive alternative to other sources of debt like bond issuances for several reasons. Many leveraged loans are issued at a floating rate. Floating rate coupons may benefit borrowers in shifting rate environments, particularly as rates decline. In addition, leveraged loan markets can often move faster than high yield bond markets when timing matters most.

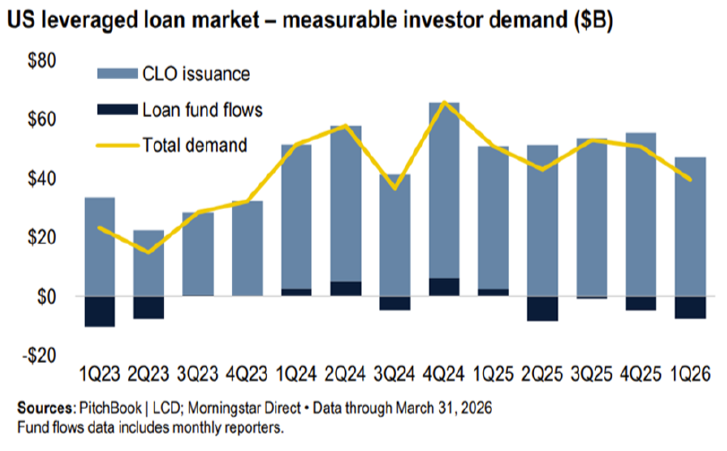

CLOs are the single largest source of demand for leveraged loans, historically accounting for 60–70% of all leveraged loan purchases.¹ CLO issuance is also crucial to loan flows and liquidity, as illustrated below, making up a significant portion of overall demand since Q1 2023.

The U.S. leveraged loan market reached $1.5 trillion in size in 1Q 2026.² Without CLO demand, we can expect that borrowing costs would rise, liquidity would contract, and capital formation for thousands of businesses would become materially more difficult.

How the CLO Structure Delivers

A CLO is a structured vehicle that pools together typically 150-250 leveraged loans and issues rated tranches of debt and equity against that pool. Each tranche has a different risk profile and priority of payment. Senior tranches get paid first and carry the least risk. The residual, or equity tranche, sits at the bottom of the capital structure and absorbs losses first. In between the AAA-rated and equity tranches are mezzanine tranches, typically AA to BB-rated,³ that offer a meaningful yield premium over investment grade bonds while still carrying structural protection.⁴

This waterfall and other structural credit protections, like collateral pledges and over-collateralization, help support more predictable cash flows that attract investor inflows and are a large part of why CLOs continue to be the leveraged loan market’s largest buyer.

Leveraged Loan and CLO’s Symbiotic Relationship

The relationship between CLOs and the leveraged loan market is largely symbiotic.

Without CLOs, demand for leveraged loans would be a fraction of what it is today due to post-financial crisis banking restrictions limiting traditional banks’ appetites for balance sheet lending. While loan mutual funds and loan ETFs make up the bulk of the non-CLO leveraged loan demand, they are subject to retail redemption pressures. CLOs, by contrast, are closed-end, term-funded vehicles that issue liabilities with fixed maturities that are not subject to redemption pressure.

For the businesses borrowing in this market, CLO demand means tighter spreads, better terms, and more reliable access to capital across credit cycles.

Implications for Investors

The leveraged loan market does not make headlines the way equities or treasuries do, but it is quietly an important source of capital for many businesses in the face of strict lending requirements.

For investors seeking exposure to corporate debt, unlike buying a corporate bond, CLOs may offer diversified exposure to hundreds of issuers with structural protections built into the waterfall and is a compelling investment for any portfolio.

Endnotes

- Pitchbook | LCD, US Leveraged Loan Quarterly Trend Lines, Q3 2024.

- Pitchbook | LCD, US Leveraged Loan Quarterly Trend Lines, Q1 2026.

- Quality ratings reflect the credit quality of the underlying securities and are subject to change. S&P/Moody’s assign a rating of AAA/Aaa as the highest to D/C, respectively, as the lowest credit quality rating.

- Palmer Square CLO BB Yield Index 2015-2025, 02/28/2026.

Past Performance is Not Indicative of Future Results

Prospect Capital Management L.P.

Headquartered in New York City, Prospect is an SEC-registered investment adviser that, along with its predecessors and affiliates, has a more than 30-year history of investing in and managing high-yielding debt and equity investments using both private partnerships and publicly traded closed-end structures. Prospect and its affiliates employ a team of approximately 100 professionals who focus on credit-oriented investments yielding attractive current income. For more information, call 212.448.0702 or visit prospectcap.com

This information is educational in nature and does not constitute an offer to sell or the solicitation of an offer to buy any securities. Prospect is not adopting, making a recommendation for, or endorsing any investment strategy or particular security. All opinions are subject to change without notice, and you should always obtain current information and perform due diligence before participating in any investment. All investing is subject to risk, including the possible loss of principal. Prospect cannot guarantee that the information herein is accurate, complete or timely. We make no representation or warranty in respect of any information derived from the third-party sources which has not been independently verified.